Boom Town

Boomflation

One reason we talk about inflation a lot around here is that the increased costs tend to fall on those who can least afford it, and the increased revenues tend to line the pockets of those who least need it. In the marketplace of ideas, it is important to keep an open mind when thinking about complex economic forces like inflation, because you never know when a new, credible argument may emerge.

Today, I give you: Boomers. Alex Yablon presents a generational take on inflation and other negative market forces in Insider:

Boomers, who were for a long time the largest generation in global history, are entering their twilight years. And as they ride off into the sunset, they're leaving behind an economy that isn't really built to accommodate the demands of the 21st century. Boomers have spent the past few decades shaping the world in such a way that has made the current crunch more painful and sets up future generations for continued deprivation.

He posits boomers have milked our roaring economy for all its worth and are now riding off into the sunset with their wealth and security, leaving a shaky, understaffed economy for the rest of us.

Employment-wise, much of the blame for rising wages has been laid upon younger workers. But that’s not the case:

The labor-force participation rate among people in their prime employment years, 25 to 54, is incredibly close to its pre-pandemic level, while the rate for those 55 and older is still down significantly. A working paper from researchers at the Federal Reserve found that a surge in retirees accounted for almost all of the decline in the labor-force participation rate up to October. A breakdown by the think tank Employ America in November found that a decline in participation by part-time workers 70 and older accounted for more than half the fall in employment of the older cohort.

Boomers leaving the workforce accounted for nearly all the changes in the last few years, with the oldest retirees making up the bulk of that drop-off. Now, it’s perfectly fine for people of retirement age to retire, but those same boomers looking forward to spending their twilight years in Florida or wherever didn’t leave the job market with enough options to replace them.

Boomers were born during a post-WW2 baby boom that ended in 1960. The boomers themselves had less children than their parents, with the birth rate falling by half over the next twenty years. This has created an unusually acute ‘sandwich’ generation among Gen X and millenials who are trying to raise their own children and care for aging parents.

One way to fill the gaps left by a declining birth rate is immigration. But! Boomers have become particularly hostile to non-white immigrants, perhaps owing to their upbringings in an America that was far less diverse. An aging, conservative-leaning generation voting for politicians who demonize and deny entry to millions of immigrants who could help replenish the labor market those same voters are leaving creates a vicious cycle of labor shortages and cost of living increases.

Then there’s the real estate market. Much has been written about boomers pulling up the ladder behind them with regards to home ownership:

In 2019, boomers, only about 22% of the population, owned 42% of American homes, and they especially dominated homeownership in coastal markets.

Though boomers are retiring en masse, they only just began selling their longtime homes, and aren't downsizing fast enough to keep up with demand.

An obsession with home ownership and real estate making up an inordinate of many boomers’ wealth means the elderly are hanging onto their houses longer, refusing to downsize, and passing them on to heirs who may be inclined to become landlords rather than selling.

Then there’s zoning. Boomers, sitting on property that may have appreciated exponentially over the last few decades, often oppose zoning reforms or proposals to build increased housing density, for fear their most valuable asset will depreciate as a result.

All of Yablon’s suggestions to fix the labor, housing, and other economic shortages created by the choices of past generations are things we’ve talked about before: more immigration, more housing density, better energy and resource distribution, and investments in infrastructure. Standing in the way of any reasonable reform that might help younger generations is, of course, our legislative gerontocracy - the average House rep is 58, while Senators clock in around 65, and our president is 80.

Inheritance

All that boomer wealth has to go somewhere, and most of it will end up inherited by their children. This is good news for Gen X and millenials, in theory:

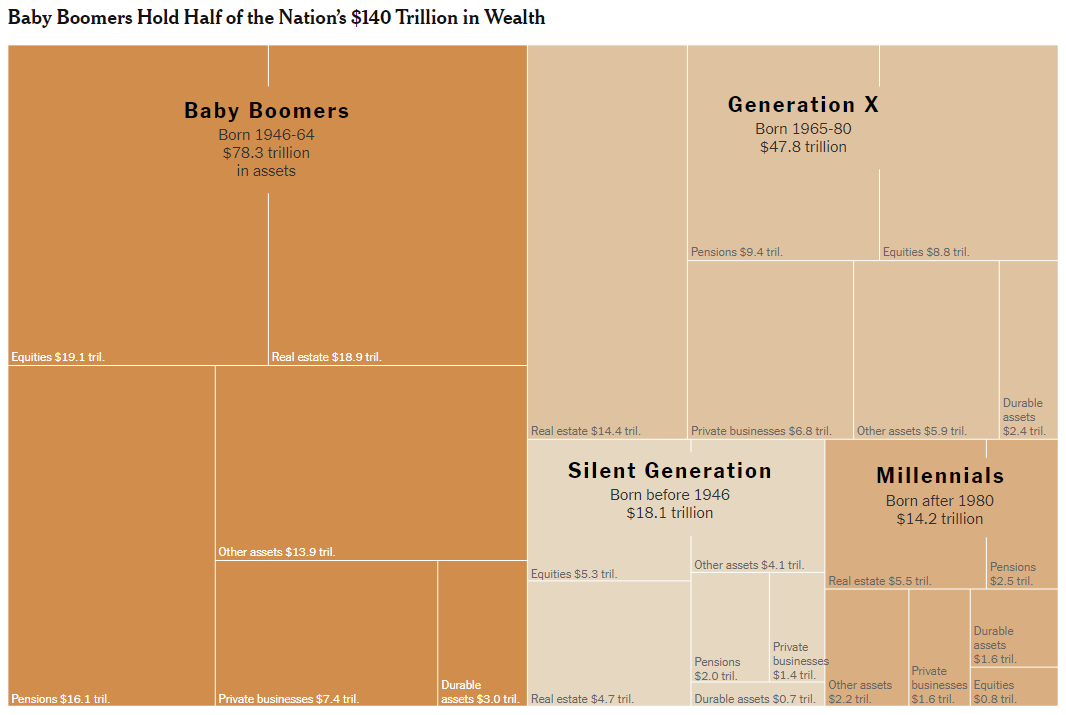

In 1989, total family wealth in the United States was about $38 trillion, adjusted for inflation. By 2022, that wealth had more than tripled, reaching $140 trillion. Of the $84 trillion projected to be passed down from older Americans to millennial and Gen X heirs through 2045, $16 trillion will be transferred within the next decade.

But, of course, most of that money belongs to the top percentiles:

The wealthiest 10 percent of households will be giving and receiving a majority of the riches. Within that range, the top 1 percent — which holds about as much wealth as the bottom 90 percent, and is predominantly white — will dictate the broadest share of the money flow. The more diverse bottom 50 percent of households will account for only 8 percent of the transfers.

Right, yes, obviously. Boomers wealth has reached such outsized proportions not only due to real estate gains, but their exposure to the stock market via holdings and retirement funds:

The average price of a U.S. house has risen about 500 percent since 1983, when most baby boomers were in their 20s and 30s, prime years for household formation.

[…]

The stock market, as measured by the benchmark S&P 500 index, is up by more than 2,800 percent since the beginning of 1983, around the time index funds took off as a mainstream investment for corporate employees and many other middle-class professionals. (Those figures do not include dividends and are not adjusted for inflation, which they have far outstripped; consumer prices have risen about 200 percent over those 40 years.)

Nice, right? You buy a house at the affordable market rates of the ‘70s and ‘80s, and watch its value quintuple by the time you retire. You amass a portfolio of inexpensive stocks and that grows thirtyfold.

Of course, only around 60 percent of Americans have a home, or own stock. And of those, only the wealthiest will be able to use tax code loopholes to hand millions of dollars to their kids essentially tax free:

High-net-worth and ultrahigh-net-worth individuals — those with at least $5 million and $20 million in cash or easily cashable assets — make up only 1.5 percent of all households. Together, they constitute 42 percent of the volume of expected transfers through 2045, according to the financial research firm Cerulli Associates. That’s about $36 trillion as of 2020 — numbers that have most likely increased since.

[…]

As a result, although high-net-worth and ultrahigh-net-worth individuals could inherit more than $30 trillion by 2045, their prospective taxes on estates and transfers is $4.2 trillion.

Seven percent tax on a multi-trillion dollar windfall? Sounds good! To put it in perspective, that $36 trillion is more wealth than the Silent Generation and millennials have today, combined:

The fact that boomers control half the nation’s wealth is both an astonishing feat of post-war American imperialism and a damning indictment of how uneven our society has become.

In theory, the boomer wealth will eventually flow to Gen X and millenials and the scales will tip back towards even. But, as we’ve addressed, that doesn’t fix our labor markets, our supply chains, our immigration policies and civil rights laws, or any of the myriad ways the boomer generation has warped the country’s politics and values to fit their FYGM attitudes. They’re literally lighting the planet on fire to hoard more wealth, when they’ve already got most of it.

One bright spot is that, unlike right-listing Gen X, millennials and Gen Z Americans are on track to be far more progressive than their elders. The downside is we’ve got awhile before the younger boomers and older Gen X die off and leave what’s left of the planet in more pragmatic hands.

Logging

| Seeking Alpha")

We’ve talked about oil companies claiming unproven carbon capture technology makes them industry leaders in the fight against climate change. I wrote:

With the billions in green energy grants floating around, it’s a good bet a lot of it will end up at the companies who set our planet alight, provided they hide the matchbook and greenwash their moonshot projects with credible-sounding economic analyses.

Another company taking advantage of those green energy bucks is Weyerhaeuser, the nation’s largest and most prolific logging company:

Although Weyerhaeuser is cutting down as many trees as ever and plans to increase lumber production 5% in the next few years, it says its net carbon footprint is negative—so much so that it is offering carbon dioxide storage capacity to other companies. Weyerhaeuser expects a new unit dedicated to helping other firms offset their emissions to generate $100 million a year in profit by the end of 2025.

How nice! They’re cutting down more trees, but because they own so many trees they aren’t cutting down, other companies can give them millions to offset their own emissions. Not that Weyerhaeuser would cut those trees down if those companies didn’t give them millions. Greenwashing!

Not content with rent seeking off their vast land holdings, the company also claims the trees it cuts are carbon offsets:

Even though lumber doesn’t continue absorbing carbon dioxide, the company takes credit for an additional 11 million tons of carbon held in those wood products. It reasons that carbon continues to be stored in the lumber after it goes into houses and other structures, which wouldn’t be the case if a tree fell and decayed on the forest floor.

Sure, why not. Building houses stores more carbon than letting trees decay naturally. I’m sure there aren’t any other benefits to plants dying in a forest, given that’s how nature has worked for billions of years.

The company has found other innovative ways to earn money off its idle property:

Weyerhaeuser already leases space on its timberlands for solar panels and wind turbines, and it sells land parcels to conservation groups. Developers can pay to restore or preserve wetlands on company land so they can build on sensitive habitats elsewhere.

Let’s examine that last sentence: developers can pay to ‘preserve’ wetlands on land owned by a logging company so they can destroy wetlands for development projects elsewhere? Am I having a stroke?

Don’t worry they haven’t forgotten about (unproven!) carbon sequestration projects either:

New ventures include carbon offsets and geologic sequestration, which will involve piping factory exhaust into porous rock thousands of feet beneath its Gulf Coast pineries.

All this greenwashing is meant to add to the company’s bottom line, but it’s also a cynical ploy to convince markets the millions of acres of land it owns around the country are worth more money and therefore its stock is undervalued:

Weyerhaeuser executives hope its climate unit will persuade investors that its land—and its shares—should be valued higher, and that it is an attractive stock for investors motivated by environmental concerns.

Of course. Because it’s not about actually slowing climate change, or reducing the amount of CO2 in the air. It’s about making numbers on a spreadsheet go up through regulatory arbitrage and relying on regulators and bankers playing along with your ruse.

Annuities

We’ve talked a bit about pensions lately in these pages. In their ideal form, pensions are a critical safety net for retirees, ensuring they don’t run out of money in their later years. Most Americans have a single pension they will end up relying on - Social Security. Due to its work history means testing, though, Social Security may not be enough to sustain a comfortable life.

Annuities are not pensions - an annuity is an insurance contract that splits up a lump sum into a series of regular payments. However! Now investment firms are offering ‘pension-like’ 401(k) annuities to their customers:

State Street and other asset managers are embedding the annuities within target-date funds, portfolios of stocks and bonds that expose younger workers to a heavy dose of stocks and gradually shift money into bonds as they age.

You may recognize ‘target-date’ funds if you’ve had the misfortune to log into your retirement accounts within the last few years. The idea of a target-date fund is the advisor will place your funds in riskier investments with higher returns (stocks) for the first X number of years and then switch over to safe investments (bonds) as you near retirement age. This can help protect retirees from sudden drops in the value of their accounts when they need to draw on them.

The problem with annuities is they are not pensions, despite what the companies pushing them claim. In fact, they are a more expensive option:

The cost of the fund is about 0.10% a year before the portfolios add the annuity and about 0.20% afterward.

And then there’s the way they’re being marketed - the banks are trying to convince employers to auto-enroll their employees into annuity plans with an opt-out, rather than opt-in option (emphasis mine):

State Street’s new target-date fund, called the State Street GTC Retirement Income Builder series, starts replacing its bondholdings with a fixed indexed annuity when the saver is around age 47. The fund is designed to be used as a default investment for workers who are automatically enrolled in 401(k) plans. (The workers can opt out.)

Ah that’s nice. I love it when my company enrolls me in a 401(k) that has a surprise annuity attached. They’re relying on a lack of financial literacy and paperwork scrutiny all too common when dealing with the unnecessary complexities of enrolling in a retirement plan at work.

Then there’s the annuity law Congress passed (at the behest of the banking industry) that contains, uh, a mildly alarming caveat:

The law protects employers that follow certain procedures from being sued if they select an annuity from an insurance company that later fails to make the promised payments.

Again, a reminder, these are insurance plans being offered as pensions, funded by our 401(k) accounts, at a higher fee. What is the point? It may sound reasonable for seniors who don’t have experiencing managing large sums of money to receive a check each month that covers their bills. But doing so via expensive, opaque insurance instruments attached to retirement funds run by for-profit banks seems like an unnecessary risk to take.

Short Cons

Science - “When neuropsychologist Bernhard Sabel put his new fake-paper detector to work, he was “shocked” by what it found. After screening some 5000 papers, he estimates up to 34% of neuroscience papers published in 2020 were likely made up or plagiarized; in medicine, the figure was 24%.”

Bloomberg - “In less than a year, the couriers flew more than 80 flights, carrying cases full of drug money. The group communicated on a Whatsapp group called Sunshine and Lollipops.”

KFF Health News - “But patients are not necessarily coming to doctors’ offices now because of the science. They are citing things they saw on TikTok, like Chelsea Handler and other celebrities talking about their injections.”

Rolling Stone - “As we approach the 20th anniversary of one of the most unjust and calamitous wars the U.S. ever waged, #Mattisisms read like a way for Americans to save face amid self-inflicted disasters that revealed their weakness.”

ProPublica - “To call the FCC’s environmental approach hands-off would be an understatement. The agency operates on the honor system, delegating much of its responsibility to the industries that it regulates.”

FT - “Given the intense scrutiny that Prigozhin has faced in recent years, there has been surprisingly little attention on his immediate family. Up until days before the Ukraine invasion, Prigozhin’s own children were able to move freely across the EU, enjoying a life of international luxury even though their father and his companies had been under western sanctions since 2016.”

NPR - “We couldn't find a single case of a police officer who reported being poisoned by fentanyl or overdosing after encountering the street drug that was confirmed by toxicology reports.”

WSJ - “Prompts to leave 20% at self-checkout machines at airports, stadiums, cookie shops and cafes across the country are rankling consumers already inundated by the proliferation of tip screens. Business owners say the automated cues can significantly increase gratuities and boost staff pay. But the unmanned prompts are leading more customers to question what, exactly, the tips are for.”

Know some boomers? Send them this newsletter! Or, maybe don’t. We don’t want them to know what we’re up to.