It Was All A Dream

Life Expectancy

We have talked before about the UK’s declining life expectancy and the US and UK’s wealth inequality compared to their peers. Now, the Financial Times - the go-to publication for quantifying human misery - has new data on US life expectancy and it’s…not good:

American life expectancy compares extremely unfavourably with the UK. The English seaside town of Blackpool has been synonymous with deep-rooted social decline for much of the past decade. It has England’s lowest life expectancy, highest rates of relationship breakdown and some of the highest rates of antidepressant prescribing. But as of 2019, that health-adjusted life expectancy of 65 (the number of years someone can be expected to live without a disability) was the same as the average for the entire US.

The British city with the worst life expectancy is the United States average. A fact made more damning by the income disparities between the two countries:

A car-wash manager in Alabama can now earn $125,000, about 50 per cent more than the head of cyber security at the UK Treasury even after accounting for different living costs.

Recent research has shed light on the ‘deaths of despair’ in America - a combination of opioid overdose, suicide and other gun deaths, and needless mortality due to poor health and lack of access to care. These reports focused on white males, who make up a big enough proportion of the US population to drag down the overall life expectancy.

What the FT and others have found, though, is even more shocking. Children in America are dying at an astonishing rate, way out of step with any other rich country:

One in twenty-five Americans will not make it to their fortieth birthday. And the epidemic of youth mortality in America is getting worse, fast:

According to that March JAMA essay, the death rate among America’s youths increased by 10.7 percent from 2019 to 2020 and 8.3 percent from 2020 to 2021. The phenomenon was more pronounced among older children and adolescents, but the death rate among those age 1 to 9 increased by 8.4 percent from 2020 to 2021, and almost none of that effect was the result of the pandemic itself.

The young were far less likely to die from COVID-19, so what gives? Guns and drugs, our two national pastimes:

Guns were responsible for almost half of the increase from 2019 to 2020, as homicides among children age 10 to 19 grew more than 39 percent. Deaths from drug overdoses for that age cohort more than doubled.

‘Homicides among children age 10 to 19’ is such an American sentence, don’t you think?

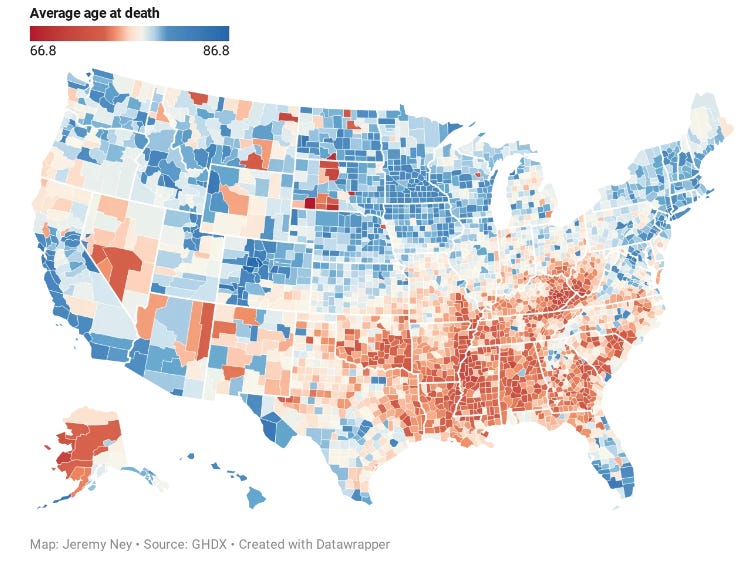

Like everything in this country, wealth inequality does, of course, play a role, but so does where you live and the color of your skin. Mortality is increasing more quickly for people without a college degree. Black Americans live five years less than whites, on average. Black men have a life expectancy so bad they’d be better off living in Rwanda or North Korea. The Deep South has mortality rates as much as twenty years lower than their Northern counterparts:

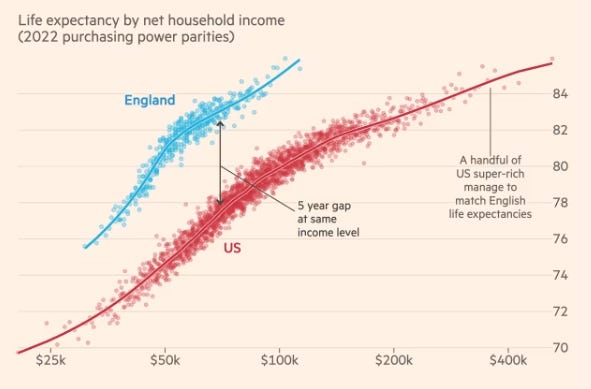

And all but the wealthiest Americans can expect to live five less years than their British counterparts:

Even making $200,000 dollars a year won’t save you from the myriad ways America can kill you. The good news, if there is any, is that if you make it to 75, you’ll probably live about as long as a Brit, which, again, is the lowest bar in Europe.

Like our dissection of American poverty, the American life expectancy crisis is a study in the ways this country finds to take from its citizens. We’ve created a society where daily life is so needlessly dangerous, where any parents can lose a child to drugs or senseless violence regardless of their socioeconomic status, and we spend most of our time defending our exceptionalism. We are indeed exceptional, just not in the way we think.

Cars

Another way Americans have found to kill themselves and the planet is giant, expensive cars. We love our fuckin’ cars. There are nearly two cars per household in America, and more than ninety percent have at least one. We’ve got eight parking spots per car, because god forbid we can’t park our big, stupid cars anywhere and everywhere.

And they are big cars. Huge, compared to any other country:

The average new American car purchased in 2021 weighed 1.94 tonnes, fully half a tonne more than the European average. Purchases of SUVs and “light” trucks together now account for four out of every five new vehicles bought in the US, up from one in five 50 years ago.

Our top selling vehicle is a pickup truck that starts at four thousand pounds and can reach fifty-seven hundred, nearly three tons. Needless to say, this is pretty bad for the environment:

And they’re really good at killing human beings:

It’s the massive, heavy cars, sure, but it’s also American driving habits, which are far more (needlessly) dangerous than our European brethren:

Almost one in 10 drivers and passengers in the front seat of US cars do not wear a seatbelt, and 45 per cent say they often drive at least 15 miles per hour above the speed limit on motorways.

[…]

The grim result is that half of the car occupants killed in the US in 2020 were not wearing seatbelts vs 23 per cent in the UK. Speeding is implicated in 30 per cent of fatal crashes in the US but just half of that in Britain.

The author estimates we’d have twenty percent less driving fatalities if we simply wore seatbelts and obeyed speed limits (which are already higher than other countries) but nah, fuck that, right? Freedom means the freedom to plow your two-ton SUV into whatever you want. Including pedestrians:

Nearly 7,400 pedestrians were killed in 2021 according to the National Highway Traffic Safety Administration, the highest figure in four decades…

US auto manufacturers continue to make pickups and SUVs bigger, which means bigger blind spots, often comically so. Our giant cars give us the impression we’re safe - and all that metal between us and the outside world does help - but giant cars with poor visibility and more screens to distract from the act of driving make anyone not inside a few tons of steel a lot less safe.

Big, heavy cars are ruining the environment, destroying our roads, and killing our people. Our obsession with cheap gas mutes incentives to make cars more efficient, though Democratic administrations do often pay lip service to better mileage. We can try forcing car companies to build more EVs, but half of Americans say they won’t buy them. We’ll keep building bigger, heavier cars to protect us from imaginary threats on the road, while speeding with no seatbelt on, maybe drunk, feeling safer than ever while the opposite is true.

Local News

If there were ever an ideal medium to convey to the average American that their cars are less safe, and their children are dying to drugs and violence, it would be the local news.

For many in TV-centric Americans, the local news is delivered in the early morning as they get ready for work, or in the evening after dinner. The central player in the consolidation of local TV is Sinclair Broadcasting, run by a family of pro-Trump conservatives. They’ve spent decades buying up the maximum number of allowed stations and networks, and milking them for profit.

Concerns about the company using its reach to push a conservative agenda aside, a recent study showed what Sinclair does above all is slash resources from its stations:

[Researchers] found the amount of news content published overall steeply declined after a Sinclair acquisition––evidence the company may indeed be depleting its newsrooms of resources, the authors said.

Sinclair reaps profits by reducing local reporting and using cheaper, syndicated content across its network. Some of it is conservative propaganda, to be sure, but the most chilling effect Sinclair’s rapacious domination of the local TV news market is to curtail local journalism from the source of news a third of the country relies on.

Then there’s the newspaper business. Alden Global Capital has been the target of journalistic ire in recent years, as the hedge fund snapped up well-known legacy newspapers across the country and viciously cut staff and costs. Alden doesn’t run its newspapers like newspapers, however, allowing circulation numbers to shrink while it extracts short-term profits and lets publications wither and eventually die.

The loss of a local newspaper has real consequences, though:

When a local newspaper vanishes, research shows, it tends to correspond with lower voter turnout, increased polarization, and a general erosion of civic engagement. Misinformation proliferates. City budgets balloon, along with corruption and dysfunction. The consequences can influence national politics as well; an analysis by Politico found that Donald Trump performed best during the 2016 election in places with limited access to local news.

Local newspapers have long fought a losing battle to hold local leaders and politicians accountable. Journalism is hard, thankless work, especially as police departments and politicians become more adept at spreading their lies online. Alden’s strategy of using newspapers and weekly publications as piggy banks to line its investors’ pockets is having the predictable side effect of making life worse for the people living in the cities it targets for takeover.

It’s not just the hedge funds, unfortunately. Gannett, a newspaper company over a century old, has turned to similar tactics in its newsrooms:

While Alden failed in its bid for Gannett in 2019, it sparked a wave of newspaper industry consolidation that some had foreseen for years. Within a few months, the two largest newspaper companies in the United States — No. 1 Gannett and No. 2 GateHouse — announced they were merging. The name would remain Gannett, but GateHouse execs were mostly left in charge.

At the end of 2018 — the last full pre-merger year — the two companies had roughly 24,338 employees in the United States and 27,600 worldwide.

[…]

And its most recent SEC filing reports that, as of the end of 2022, Gannett had just 11,200 U.S. employees remaining (plus another roughly 3,000 overseas).

In other words, Gannett has eliminated more than half of its jobs in the United States in four years. It’s as if, instead of merging America’s two largest newspaper chains, one of them was simply wiped off the face of the earth.

Gannett cited declining newspaper revenues, but it cut overhead faster than necessary because the company had taken out a massive loan to fund the merger:

In Q4 2022, digital subscriptions at Gannett newspapers — all of them — brought in a total of $35.5 million. But the company spent more than that, $47.3 million, just on debt payments.

We talk a lot around here about the financialization of everything, and all the negative externalities it causes. In this case, Gannett undertook a merger it likely knew was going to be harmful to its business - newspapers - but caved to market pressures and corporate greed. As a result, it’s had to cut fifteen thousand jobs, and its papers saw outsized circulation declines as it struggled to pay its outsized debt.

An estimated one million people cancelled their subs to Gannett newspapers between 2018 and 2022, which is one million readers in major US metro areas who are now getting their news elsewhere - likely Facebook. Even Gannett’s powerhouse USA Today lost hundreds of thousands of subscribers. Even if we can’t draw a straight line between editorial and newsroom cuts and precipitously falling readership, it’s certainly exacerbating an ongoing problem. Gannett isn’t trying to improve the newspaper business, it’s trying to wring every last penny it can before the ship sinks.

Politicians, corporations, and anyone who feasts on the carcass of systemic corruption stand to benefit from less scrutiny. Threadbare newsrooms mean fewer pesky reporters to expose their misdeeds. Alden is a hedge fund, and may view its hollowing out of the business as an added benefit. But Sinclair and Gannett, two actual news companies, are perpetuating the same outcome, for the same venal reasons. A less informed America is a more compliant America, which is the end goal of its powerful, moneyed elite.

Home Prices

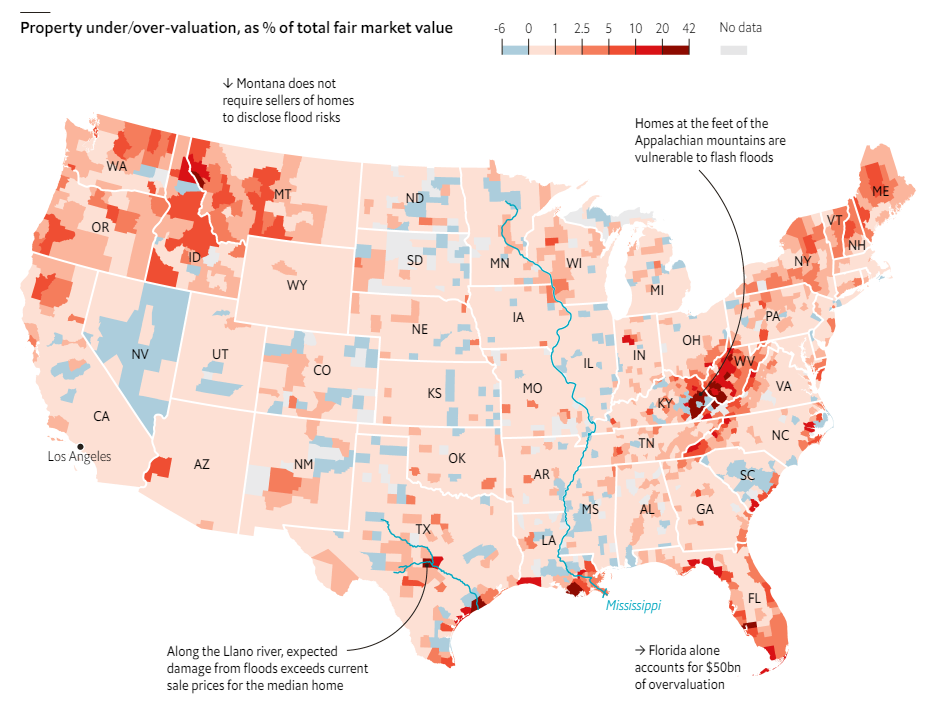

For most Americans, the primary source of their wealth is their house. Relatedly, did you know our level of home ownership is abysmal by worldwide standards, far behind countries like Latvia, Bulgaria, Kenya, and Vietnam? Anyhow, the homes Americans do own tend to be quite valuable compared to our peers, but a sober analysis of our housing market tells another story: we’re papering over high levels of expected losses through property damage to prop up prices. How high?

One study in 2021 estimated this overvaluation at $33bn-56bn. But a new paper in Nature Climate Change, whose lead author is Jesse Gourevitch of the Environmental Defence Fund, an advocacy group, puts it at $121bn-237bn, with a central estimate of $187bn.

Much of this is due to overpricing of houses in flood-prone areas. Like, you know, Florida, which accounts for an estimated fifty billion in price bloat:

We often associate flooding with big hurricanes, but homes in Appalachia, New England, and Montana can be flood prone because they lack proper infrastructure or drainage.

Flood insurance is issued by the government, which, because it’s the government, can offer underpriced policies to homeowners and paper over any eventual losses:

…in 2017 Congress forgave $16bn of the National Flood Insurance Program’s debt.

Uninsured homeowners often make up the shortfall during disasters - many homeowners in flood prone areas are not aware they need flood insurance, or the cost of repairing their expensive homes exceeds the program’s limits.

In a rational market - like the one economists continue to insist we have - home prices would be tempered by estimates of long term disaster risk and damage. But, because we live in AMERICA, that doesn’t happen, and at-risk homes continue to be bought and sold with wild abandon, loading the costs of bailing out regions hit by storms onto taxpayers who haven’t chosen to live in a swamp.

Florida, in particular, is at such acute disaster risk that its state government is straining under the weight of claims and insurers going out of business. Last year it passed insurance reform measures to essentially prevent its entire property market from imploding:

Florida insurers faced more than 100,000 lawsuits last year claiming $7.8 billion in damages, while the other 49 states faced a total of 24,700 claiming $2.4 billion.

Some of the lawsuits were due to the state’s perverse claim system, but some was (of course) scam related:

An avalanche of lawsuits fueled by roofing scams has plunged Florida into a property insurance crisis that has forced dozens of companies to shut their doors, drop customers, raise rates or flee the state. It’s a slow-motion collapse that lawmakers have known about for years but have failed to fix.

Florida is especially vulnerable to the ongoing effects of climate change (which its leaders deny exists):

Insurers are also struggling to price legal risks and had underwriting losses exceeding $1 billion each of the past two years. More than a dozen insurers have failed since early 2020 while a growing number are pulling back from the market because they can’t get reinsurance.

Florida has, in its free market wisdom, pumped funds into its state-backed insurance entity offering homeowners…below market rates:

Homeowners have increasingly turned to state-backed Citizens Property Insurance Corp., which offers below-market premiums.

Which the state’s governor admits miiiiiiight be insolvent:

Florida Gov. Ron DeSantis raised some questions Friday when he suggested that Citizens Property Insurance Corp., the state-created insurer, has “not been solvent” and may be unable to pay all claims from a major hurricane.

So, yeah. One of the nation’s hottest property (and rental) markets, with home values ascending into the stratosphere, rests upon a (very) insolvent property insurance fund, which offers below-market rates to convince homeowners their house is both 1) worth a lot of money 2) safe from disaster, neither of which are technically true. At the state, local, and national level we are all subsidizing the poor purchasing decisions of a deluded sliver of the population who insists on building houses in low-lying flood basins and shorelines, confident they’ll continue to be bailed out while their homes appreciate at double-digit rates.

It’s a perfect metaphor for the American dream - the freedom to do exactly what you want, with no regard for the safety of yourself or others, and be richly rewarded for it.

Short Cons

NBC News - “The officials were paying for the whiskey, which can cost thousands of dollars a bottle, but they had used their knowledge and connections at the commission to obtain them, and consequently deprived members of the public of the spendy booze, the investigation said.”

OCCRP - “Across the globe, shadowy groups of cyber mercenaries have been harnessing digital technology to hack elections, employing their dark arts for anyone willing to pay a hefty fee to subvert democracy.”

Bloomberg - “The fix has been in on handball matches. Triathlons and biathlons are worried about fixes. Organized crime has targeted kabaddi matches in India. Lots of betting now whirls around table tennis, volleyball and cricket.”

The Markup - “Many grocers systematically infer information about you from your purchases and “enrich” the personal information you provide with additional data from third-party brokers, potentially including your race, ethnicity, age, finances, employment, and online activities.”

WSJ - “Using a remarkably low-tech trick, thieves watch iPhone owners tap their passcodes, then steal their targets’ phones—and their digital lives.”

POLITICO - ““Santos taught me how to skim card information and how to clone cards. He gave me all the materials and taught me how to put skimming devices and cameras on ATM machines,” Trelha said…”

Bloomberg - “Provence asked Gallagher for more information. But by then, unbeknownst to her, her investment was already all but gone—along with tens of millions of dollars more from hundreds of other investors.”

Know someone buying a house in Fort Myers, or a Cadillac Escalade, or planning to retire at 75? Send them this newsletter!