Money in the Bank

Banking 101

- YouTube")

For most people, banking is a relatively simple transaction. You deposit your money into a bank account, the bank holds onto that money, maybe pays you a small amount of interest on it, and when you need to take the money out the bank gives it to you, or transfers it to someone else on your behalf. This is, loosely speaking, how retail banking appears to work for the majority of the population. But! It is not how banking actually works.

When you deposit funds into a bank, you are in fact loaning the bank money, which it can then use for other things. I have heard the phrase ‘banks create money to lend into the economy’ a lot lately, and it is a bit brain-breaking because while we do not spend time thinking about how new money enters the economy, that indeed what banks actually do. When I deposit my five thousand dollar paycheck into my bank, I’ve given the bank five grand worth of capital to lend against, and I’m technically a creditor of the bank, to the tune of five grand.

So, in a way, everyone depositing and keeping their money in banks is what keeps new dollars flowing into the economy, being lent to businesses or homeowners or used to make investments for the bank that it believes will yield profits, and all is generally well.

The thing is, banks use our money as leverage and lend or invest many times as much as we give them. If a bank is expected to keep, say, a ten percent capital margin on hand against its liabilities - my five grand is a liability - that means it can lend out $4,500 out after I put it in. If I come back and withdraw the full five grand, it’s going to pay me with my $500 and a bunch of funds from other people.

This is reductive, but you get the point. Retail banking is not simply taking in funds, earning interest on those funds, and hanging onto those funds in case we need them back. It’s about leveraging those funds to do lots of other stuff that, presumably, powers the economy, however we define that.

This function - banks creating money to fuel economic growth - is so important that in 1933 the US passed a Banking Act that created the FDIC which guaranteed everyone’s deposits up to a certain amount, so that no matter what dumb shit the bank did with your money, the government would make sure you got it all back. The bank could buy $4,500 worth of magic beans with my deposit, but Uncle Sam would make sure I got paid back if anyone tried to plant the beans.

Doesn’t this system seem a little…nuts? Why are we, the schlubs working jobs and depositing our earnings into our bank accounts, funding billions of dollars’ worth of loans and investments and other shit? Why does my meager paycheck go to originate mortgages to someone buying a house on a flood plain in Florida? Why, if my money is so valuable to the bank, am I paying monthly fees, and transfer fees, and overdraft fees, and getting relentlessly hammered by the bank’s marketing department to open up credit cards and savings accounts? We don’t get any of the profits when a bank has a banner year, or makes smart loans or investments. Those go to the bank’s executives and shareholders. But they’re doing it with our money, in some loose sense. That sucks!

Finance writer Matthew Klein has an excellent quote about what modern banks have become:

Banks are speculative investment funds grafted on top of critical infrastructure.

Yes! Banks are taking wild risks with a majority of the money we’re giving them, but the losses are socialized - if they fuck up, the government picks up the tab.

Klein goes on to posit that retail banking is a public good, and should not be in the hands of for-profit bankers:

Money and the payments system are public goods. Banks could focus on (what should be) their core competency: identifying creditworthy borrowers and making profitable loans.

Right. Rather than doing what they do now - taking a bunch of deposits, and creating complex and opaque financing systems to convert those into investments or loans or whatever - they could simply do all the finance stuff on their own, with their own capital, and let the rest of us bank at the Post Office or Fed Bank or whatever we wanted to call a government body whose sole responsibility would be to take our deposits and not lose them.

A question we ask often around here is - how did things get this way? Banking was not always a highly-leveraged arms race between behemoth institutions more concerned about shareholder returns and esoteric financial products than investing in their communities. Let’s dig in.

Regional Banks

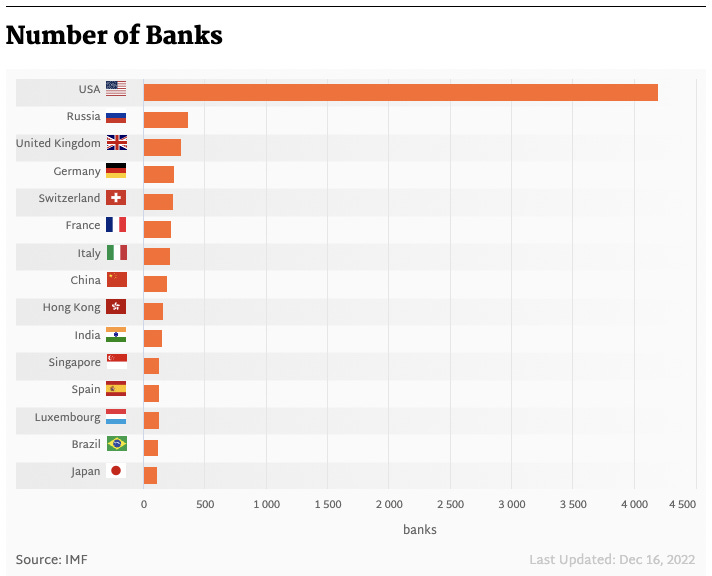

If you had to guess how many banks were chartered in America, how many would it be? A hundred? Four hundred? If you guessed more than four thousand congrats, you win! A few hundred banks sounds like a reasonable number, and the rest of the world agrees:

Why does America have so many banks? The answer is that for a very long time our country relied on regional and community banks, who took deposits and issued loans, mortgages, and generally invested back in their communities. In 1994, there were 12,500 community banks controlling around half of the industry’s assets. With so many localized banks, states had strict regulatory authority over them, and could constrain their size and behavior. Then, the Clinton administration passed legislation allowing banks to open branches across state lines and spawned a wave of megabank mergers.

Then, in 1999, Congress replaced the Depression era Glass-Steagall act with the Gramm-Leach-Bliley Act, which allowed banks to participate in commercial, retail, and investment banking under the same roof. From 1933 to 1994, retail banking had been a relatively dull business - accepting deposits to make loans back into the community. Bankers worked with customers who may have been their neighbors, and banks couldn’t take deposits and bet on, say, wildly leveraged mortgage securities or anything like that.

From that point, it took a mere 9 years for banks to blow up the global economy by using deposits and other assets to make risky bets on mortgages, insurance for mortgages, and bundled mortgage securities, all while using their lending businesses to hyperinflate a housing market, often relaxing lending standards in pursuit of more leverage and, concurrently, more profits.

This is not to let regional banks off the hook entirely, or claim they’re definitionally better than the megabanks - though they haven’t ever managed to take down the global economy. There was the Savings & Loan crisis in the ‘80s and ‘90s in which a bunch of community banks (called ‘thrifts’ at the time) took on risky investment strategies to combat the Federal Reserve hiking interest rates to combat inflation. They had been deregulated under Carter and Reagan, and allowed to issue riskier loans and grow their deposit base to avoid regulatory scrutiny.

Does any of this sound familiar? A bank with a localized customer base, lobbying to avoid burdensome regulations, taking risky bets during a period of rising interest rates that puts it in a bad financial situation, leading to a bank run? Haha, no, of course it doesn’t.

Silicon Valley Bank

This stroll through the history of banking and bank crises in the US is in service to last month’s news - the bank run and subsequent implosion of Silicon Valley Bank, or SVB.

The simplified story is that SVB catered to a very insular, herd-like group of depositors in Silicon Valley startups, VC funds, and associated entrepreneurs. Many of its clients held far more than the $250,000 dollar insured limit provided by the FDIC, so when word got around the bank was teetering financially, they all rushed to the exits and sparked a bank run.

SVB could probably have avoided the crisis, and many different companies and agencies warned the bank its investment strategy was risky in the face of rising interest rates. The bank had taken most of its deposits and invested them in long term treasury bonds, which on paper is just about the safest way to turn a modest profit. The problem was, those bonds lost value if they had to be redeemed early, because interest rates had gone up. If SVB was sitting on a bunch of 5-year bonds paying 3%, for example, and interest rates went up to 5%, their bonds would be worth less on the open market if they had to sell before maturity, because no one wants to make 3% when they can make 5% somewhere else.

Why would SVB be forced to redeem its bonds before maturity? Because many of its tech industry depositors were also getting slammed by high interest rates, which caused a slowdown in investment and a decrease in their (often wildly inflated) market values, which meant companies that had become accustomed to piles of nearly free cash were now burning through their reserves, which were at SVB, which meant they started withdrawing more cash, which oops oops oops.

It all seems a bit nuts, right? SVB made some interest rate bets with depositor cash, and they went sideways, and people panicked in the group chat and did a bank run, and the government stepped in to take over SVB, zero out its shareholders and executives, and sell it off to another bank. Some SVB insiders claim they were literally hours away from arranging a rescue package with government lenders, but they missed a couple key cutoffs due to time zones. The problem, of course, is how do you let your $120 billion dollar bank get to the point where a missed deadline turns it into a ghost ship, and also why are there seventeen different government lending facilities you can sidle up to and get a $20 billion dollar loan from (if you do it before 4pm)?

Why do we have so many layers of financial shenanigans to run a banking system that, for fifty years, was comparatively straightforward? The answer is because for every loan, every bit of risk and arbitrage and fiddling the bankers do with money lent against the billions of dollars’ worth of depositor money, finance gets a cut. They take a few basis points here and there and before you know it, they’ve made $275 million dollars in net income and their executives get big bonuses, etc. Until someone brushes the wrong card, and the whole house collapses.

We can talk about SVB’s questionable sales tactics or obsequiousness to the tech and VC industry, but the reality is it was a community bank in perhaps the truest sense, set up to serve a specific community of weird libertarian psychos who, at the first whiff of trouble, shanked it and left it to bleed out in the gutter.

Returning to Klein’s statement - that banks have become dangerously risky appendages on top of the critical service of keeping peoples’ cash safe - SVB should stand as a shining example of why we need to disentangle holding depositor cash and using it to make loans and investments, no matter how safe. Even the least-risky option a bank can take to attempt to turn liabilities into profits can go wrong, so the obvious fix is to simply take it out of their hands.

Banks would still have access to the billions they need to write mortgages, make investments, etc. Here is an interview with a scholar who Biden nominated to run the OCC but whose ‘extreme’ views - like the idea of taking retail banking away from banks and giving it to the Fed - got so much pushback from the bank lobby she withdrew her nomination. There are many, reasonable ways to disentangle depositors and retail banking from loan generating and investment banking, but the banks have become so addicted to the leverage depositor funds provide them - now even more safely backstopped by the government - they will vehemently oppose any change to the status quo, and their safe profits.

Other Banks

Two other bank failures happened in the last few weeks, too. Signature Bank, which had embraced crypto startups enthusiastically, caught a stray and was shut down along with SVB. The FDIC determined Signature was at similar risk - crypto bros precipitating another bank run - and took proactive action to shutter the bank. Prior to its pivot into crypto, Signature mostly made loans to real estate developers.

Unlike SVB, Signature appears to be kaput, with the FDIC prepared to auction off some $60 billion dollars’ worth of Signature’s real estate loan book, though investors are disparaging its rent-stabilized residential loans as ‘toxic waste’ which, cool. The most amusing quote about the bank’s collapse came from Barney Frank, former Congressman and one half of the Dodd-Frank Act which, ironically, sought to rein in banks after the 2008 crisis:

“I worked as a member of Congress for a certain objective,” Frank said in an interview with the Financial Times. “And then having retired, not having a pension by my choice, not wanting to be a lobbyist for reasons personal, I need to make some money.”

The guy whose signature legislation was banking regulation went to work for a bank that pivoted into crypto. What a world. Oh, and Frank ‘argued’ (not lobbied!) for the lowered capital threshold caps that allowed SVB and Signature to take on massive deposits and liabilities without increased regulatory scrutiny.

Next was Credit Suisse, the embattled Swiss bank that had endured a nearly endless series of scandals in the last few years. Swiss regulators decided that Credit Suisse should be sold to UBS for a few billion dollars and have its management team wiped out and its shareholders given a seventy percent haircut.

By all accounts, Credit Suisse wasn’t in danger of collapsing, and it had a reasonably stout balance sheet. But! The problem was its market value kept slipping, which meant the equity cushion between its assets and liabilities - essentially what the bank is ‘worth’ to shareholders - got smaller and smaller, and that made Swiss regulators nervous. The market didn’t like Credit Suisse, perhaps because the bank has spent the last few years embroiled in scandals. The market didn’t have confidence in CS’s repeated restructures, or its self-dealing plan to spin off an investment division run by one of its board members.

A bank with a diversified loan book and sufficient assets was done in by things not directly related to money management. Its executives made some stupid bets, its traders did some dumb shit, and the market said ‘ehhhh we’re not going to value this stock at 100% because we don’t trust what the bank says’ and poof, the bank is teetering on the brink of insolvency due to vibes. Maybe they were earned vibes, to be sure, but vibes nonetheless. It was less an indictment of the bank’s balance sheets than it was the bank’s governance. In a world where banking is more about shareholder perception than, you know, actual banking, perception is all that matters.

I. Ask. Yet. Again. Why should Credit Suisse, or UBS, or Chase, or any of these banks be allowed anywhere near deposits? They could simply do investments and loans and all the stuff banks used to do, when they weren’t allowed to comingle deposits and investments. A lot of bad shit happened between 1933 and 1999, but I don’t think anyone would list ‘banking’ as a major systemic problem begging for a fix. But the financiers won, and created their own private casino where they could turn deposit dollars into billions in profits, and the rest of the world has come to accept that as a necessary evil for economic growth.

Modern banking is the way it is because we’ve decided banks and bankers should be allowed to make outsized profits on our money, while paying us essentially nothing for the privilege, and while running the risk they may fuck it all up and we may need to step in and give the banks more of our money via the government to bail them out. It’s an insane system, and one we could fix relatively easily, but it seems unlikely some of the richest, most powerful people in America will hand over the keys to their money printer.

Short Cons

Rolling Stone - ““I was on a date with a girl I’d met on another app, was sitting down, she finds out I work for Trump in the White House,” Huff laments. “She’s not like, ‘Oh that’s cool, let’s talk about it.’ She literally got up and left after two minutes. So this is a real phenomenon.””

The Current GA - “Rather than seeing the company as a force for good, a growing consortium of lawmakers, religious leaders and consumer advocates believe TitleMax, and its industry writ large, to be predatory leeches on the growing ranks of working-class Americans.”

The Atlantic - “By effectively barring foreign competitors from transporting goods between U.S. ports, the Jones Act has predictably inflated the cost of shipping and shipbuilding in the United States.”

HuffPost - “Amazon spent more than $14.2 million last year on outside consultants whose job was to convince workers not to unionize, according to new disclosures filed Friday with the Labor Department.”

Know someone in banking who’s thinking about using customer deposits to make foolish long-term bets on interest rates? Send them this newsletter!