Sinkholes

Sewers

Bucks County, in the suburbs of Philadelphia, is selling its public sewer system to a private company for $1.1 billion dollars:

The Bucks County Water and Sewer Authority (BCWSA) voted 3-1 on Wednesday to give Aqua the exclusive right to negotiate a sale for a year. If it accepts Aqua’s formal offer, it would be the largest privatization ever of a U.S. public wastewater system, and is potentially transformative for Bucks County, which would receive close to $1 billion in proceeds after the authority’s wastewater system debt is paid off. The net proceeds would amount to about five times Bucks County’s annual tax revenue.

Five years’ worth of revenues seems good, right? Well:

Under Aqua’s proposal, current sewer rates would be frozen for a year. But in the coming years, rates would eventually increase to match Aqua’s rates, which are now about $88 compared with BCWSA’s average monthly rate of $48. The precise impact is unclear because BCWSA suggests that some of the sale proceeds could be used to soften the rate impact.

So, after a year the sewer costs would start rising, nearly doubling over time. And, the county would then spend some of the money to…help customers pay their sewer bills? What?

Cities and counties have been selling off public assets for cash infusions for years - the most infamous is the Chicago parking meter debacle, which will make its Arab owners billions more than the deal was worth. Rather than properly fund infrastructure, states come up with gimmicks to plug budget holes:

The deal is the latest privatization undertaken in Pennsylvania since the state in 2016 passed new rules encouraging private ownership of public water and sewer systems, which has generated a surge in private investment in water and wastewater systems, and a corresponding increase in utility rates. In essence, utility customers are financing an influx of cash to local governments.

The law, Act 12, allows private buyers to pay a higher “fair-market value” for a municipal utility and recover the cost in future rates, making it attractive for local officials to divest their unwanted systems to balance their budgets and stave off tax increases. The law’s rationale was to encourage consolidation of sometimes troubled water and sewer systems that are a threat to health and the environment. Local officials say that profit-making private owners are more capable of operating complicated water and wastewater systems.

The problem is that these ‘local officials’ aren’t liable for what happens to customers of these privatized utilities. Bucks County is only selling its sewer - so what happens when a sewer line breaks and damages water infrastructure, still managed by the public authority? Who’s responsible for all the repairs that inevitably come with an aging sewer system?

Cities and states are moving to sell off critical infrastructure rather than raising taxes to pay for necessary upgrades, because raising taxes pisses off voters, but allowing private companies to gouge customers years down the road is fine with them. Just ask Texas voters, who are poised to reelect the governor who has pushed deregulated markets and saddled them with massive utility bills, and put them on the hook for billions in debt raised to pay off the same companies.

Three Arrows

Since April, crypto markets have shed around 1 trillion dollars’ worth of value. Bitcoin and Ethereum have lost more than half their value since January. If crypto investors were anything like stock investors, they’d be the ones bearing these losses - if your coins are worth X, and their value drops to Y, you still have Y in assets. However, crypto is nothing like stock investing, because many crypto exchanges advertised themselves like banks - we’ve talked about this before - offering huge returns if people deposited their coins. The disconnect seems to be that while exchanges used words like ‘deposit’ and ‘interest rate’, they were actually behaving more like high risk hedge funds - taking customer assets and loaning them out or investing them in risky projects.

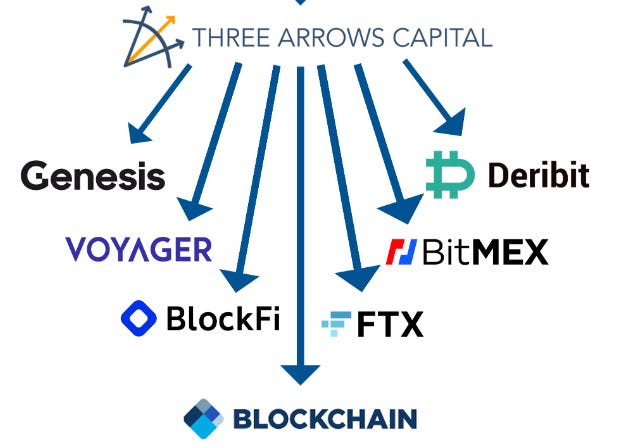

The crypto hedge fund at the center of the recent maelstrom is Three Arrows Capital, or 3AC. Here was their business model:

Three Arrows’ strategy involved borrowing money from across the industry and then turning around and investing that capital in other, often nascent, crypto projects.

Problem was, they borrowed a lot of money - billions - from exchanges all around the world, and invested it in things like Terra:

3AC told the Wall Street Journal it had invested $200 million in Luna. Other industry reports said the fund’s exposure was around $560 million. Whatever the loss, that investment was rendered virtually worthless when the stablecoin project failed.

This, combined with the market collapse of crypto more broadly, meant 3AC could no longer pay back its loans, and it started receiving margin calls:

Crypto exchange Blockchain.com reportedly faces a $270 million hit on loans to 3AC. Meanwhile, digital asset brokerage Voyager Digital filed for Chapter 11 bankruptcy protection after 3AC couldn’t pay back the roughly $670 million it had borrowed from the company. U.S.-based crypto lenders Genesis and BlockFi, crypto derivatives platform BitMEX and crypto exchange FTX are also being hit with losses.

3AC is currently undergoing bankruptcy proceedings, which are going well:

The founders of bankrupt crypto hedge fund Three Arrows Capital haven’t been cooperating in the firm’s liquidation process and their whereabouts were unknown as of Friday, according to court papers.

Typically when a financial institution goes bankrupt, the owners go to court and negotiate a settlement, or their lawyers do, but typically their creditors know where they are or how to reach them. Not so in crypto!

The hedge fund’s liquidators traveled to Three Arrows’ office address in Singapore in late June in an attempt to track down the founders, according to court papers. It appeared dormant: the door was locked, computers were inactive and mail was stuffed under the door.

Anyhow, a court in New York is now trying to oversee the liquidation of a Singapore-based crypto hedge fund incorporated in the British Virgin Islands. Good luck to everyone involved.

Luna

Speaking of Terra/Luna, its founder has been busy:

Mr. Kwon has championed the launch of a new version of Terra, the blockchain network that underpinned the failed TerraUSD and Luna cryptocurrencies. TerraUSD was a so-called stablecoin designed to maintain its value at $1, but the coin is now valued at less than a penny. Its collapse triggered a plunge of more than 99% in Luna, the cryptocurrency that backed TerraUSD’s link to the dollar.

So, in late May, Kwon launched a new token called Luna, and renamed the old one Luna Classic, because you can just do that I guess. Holders of the old Terra and Luna (Classic) tokens were given a new Luna tokens, and then those lost most of their value:

So far it hasn’t gone well: The new Luna began trading at $18.87 on May 28, tumbled right away and was recently trading at $1.97, according to data provider CoinGecko.

“I don’t understand why anybody in their right mind would want to invest in Luna 2 after watching Luna 1 blow up so dramatically,” said Mati Greenspan, founder of crypto research firm Quantum Economics.

Yeah, I don’t know. The collapse of Terra triggered the collapse of lots of crypto companies, so why not try and chase those losses by investing with the guy who caused it? My head hurts.

Theranos

We’ve talked a lot about Theranos and Elizabeth Holmes over the years. Now, the trial of her former business and romantic partner Sunny Balwani has wrapped up and he’s been found guilty on all counts:

Jury deliberations stretched for four full days following a lengthy trial that got underway in March with opening statements. A jury of five men and seven women determined that Balwani had defrauded both patients and investors, finding him guilty on all 12 charges he faced, which included ten counts of federal wire fraud and two counts of conspiracy to commit wire fraud.

You may remember that Holmes was only found guilty on four counts, and her sentencing was delayed pending her cooperation in the Balwani case, which was severed from hers when her defense team claimed they were going to use Balwani’s alleged abuse of Holmes as a defense - which they didn’t, really.

Was this all a clever legal strategy to allow Holmes to plead her own case, separate from Balwani, and then use her cooperation to cut a deal for a shorter sentence if she was found guilty? I mean, all those things happened, but it’s impossible to know whether Holmes’s lawyers - who, ironically, were likely paid for out of Theranos’s remaining funds as part of her executive agreement - were playing 4D chess, or whether things seem simply to have worked out in her favor. Anyhow, Balwani faces up to 20 years in prison and potentially millions in fines, and Holmes is at the mercy of a judge when sentencing happens in the fall. That means we only have to talk about Theranos one more time before we can put Silicon Valley’s highest profile fraud case behind us.

Short Cons

CBS News - “The Justice Department on Wednesday announced charges against three dozen people who are accused of orchestrating health care fraud schemes across the country, with laboratory owners and company executives among those accused of ordering unnecessary or fraudulent medical tests and equipment worth $1.2 billion.”

WSJ - “Amazon.com Inc. said it filed a lawsuit against the administrators of what it says are more than 10,000 Facebook groups used to coordinate fake reviews of Amazon products.”

Bloomberg - “An audit of the technology done by Chicago’s Office of Inspector General last year found that of the more than 50,000 ShotSpotter alerts for probable gunshots, only 9.1% resulted in evidence of a gun-related offense.”

Tips, thoughts, or sane public infrastructure management to scammerdarkly@gmail.com