Sunset Provision

Retirement

| The Motley Fool")

One major driver of inequality in America is wealth concentration within families, passed down via inheritance. Older generations were able to save and acquire wealth due in large part to stable employment, subsidies to (white) homeowners, and low cost of education. Obviously, less and less of these opportunities are available today, as labor unions remain marginalized, higher education has become more expensive, and lack of earning power means younger generations without family wealth are unable to buy homes.

Stable employment in prior generations might have involved a pension plan, a guaranteed retirement fund that increased over decades of work. These days, unless you work for the government, you probably don’t have a pension, or know anyone who does. Pensions are often the flashpoint in large corporate bankruptcies, and workers often get screwed when companies (or cities) don’t fund them properly.

What happened? In 1978 Congress passed the Revenue Act, creating a provision - Section 401(k) that allowed employees to defer compensation from bonuses or stock options. In 1981 the IRS decided to extend the carveout to include salary as well. Forty years later, most private industry workers in the US have a 401(k) plan as their primary source of retirement savings.

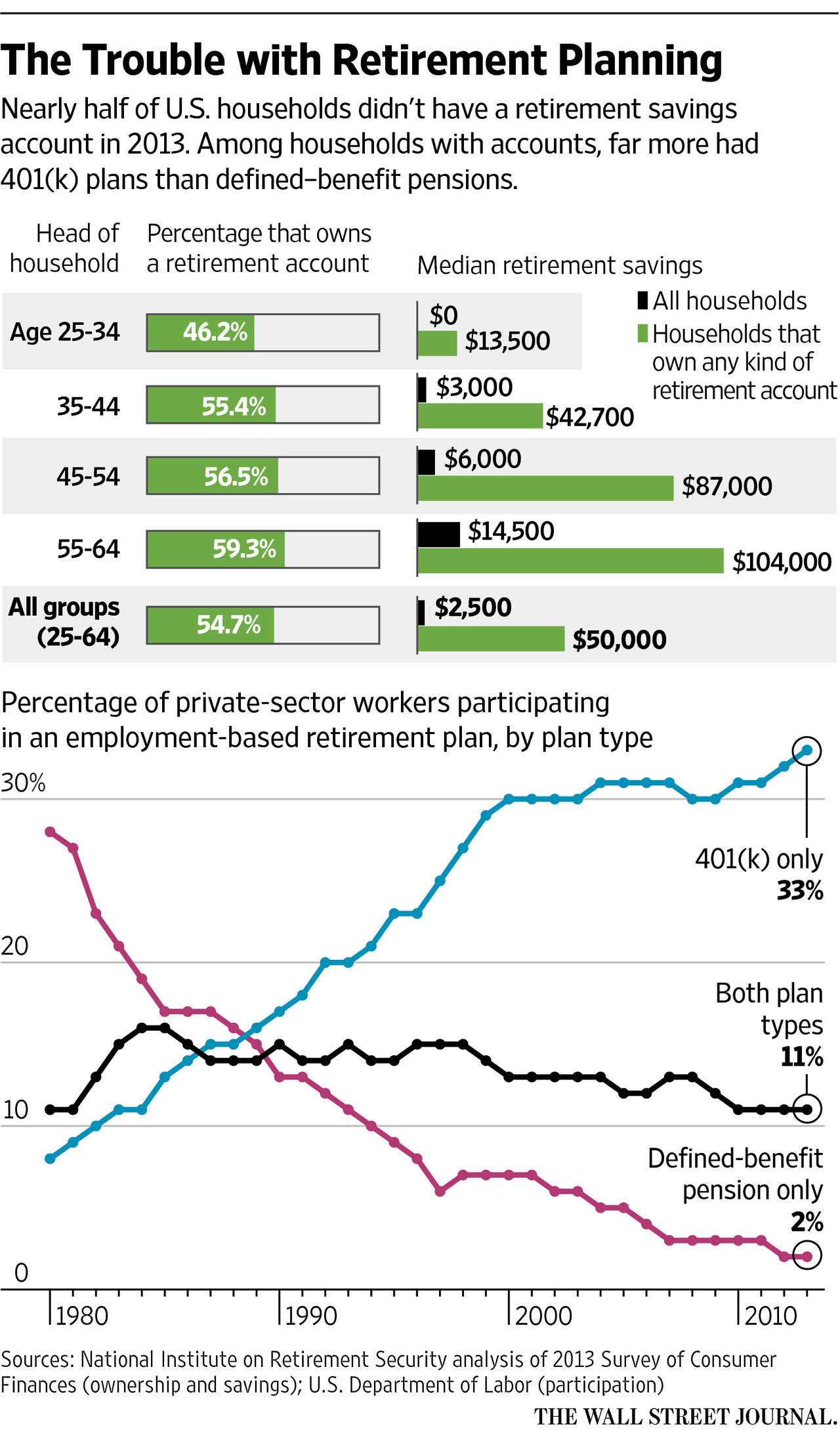

The problem with a 401(k) is that, unlike a defined benefit pension, it goes up and down with the markets, which have not exactly been stable over the last couple decades:

Many early backers of the 401(k) now say they have regrets about how their creation turned out despite its emergence as the dominant way most Americans save. Some say it wasn’t designed to be a primary retirement tool and acknowledge they used forecasts that were too optimistic to sell the plan in its early days.

[…]

“The great lie is that the 401(k) was capable of replacing the old system of pensions,” says former American Society of Pension Actuaries head Gerald Facciani, who helped turn back a 1986 Reagan administration push to kill the 401(k). “It was oversold.”

An important difference between a 401(k) and a pension is that in most cases, some or all of the money being contributed is employee earnings, meaning it’s deducted from a worker’s total compensation rather than additional money paid by the employer. Some companies offer a ‘match’ or pay the entire contribution, but retirement plans are often a perk or incentive of a job, which means that any time a worker changes employment their contributions, and often the financial institution in charge of their plan will change.

Companies love 401(k)s because their obligations begin and end with an employee’s tenure. Pension plans require employers to budget decades into the future and pay all workers past and present, whereas 401(k)s can be run through simple accounting software, adding or subtracting figures to the month’s payroll.

Another problem with 401(k)s is timing. If you happened to turn 65 in, say, 2009, you might see decades’ worth of gains wiped out by a global recession. Personally, I watched my retirement funds lose nearly five years’ worth of gains over the last six months as the markets whipsawed due to circumstances firmly out of my control. Fortunately for me, I won’t need those funds for decades to come, and compound interest should eventually accrue to a point where my meager nest egg is less susceptible to Wall Street vibe shifts.

Problem is, many younger or lower paid workers without guaranteed contributions simply don’t create or maintain retirement accounts:

Barely half of Americans have any sort of retirement account, and even those who do have an average of fifty grand saved for a potentially decades-long retirement. Not great! If more Americans had defined-benefit pensions, along with Social Security, they might have a shot at comfortable retirement. But we love our bootstraps in America, even if it means sacrificing wages during our healthy years and gambling on whether markets will be on the upswing when we’re too old to keep working.

Stocks

One group of people who love 401(k) plans is bankers. The fifty-four percent of Americans with retirement plans are paying fees to fund managers, often significantly higher than they should be. Vanguard, the inventor of the index fund and a popular retirement fund manager, generally charges the lowest fees across its accounts, but there’s no guarantee an employer will work with Vanguard. Those fees can add up - John Oliver did a show on the topic six years ago - which is simply needless transfer of employee earnings to fund managers who provide no real benefit over just slamming your money into a boring Vanguard index fund.

Another thing retirement funds do is own stocks, lots and lots of stocks. Fidelity and Vanguard alone have nearly $18 trillion dollars under management. That is a lot of stocks (and bonds!) Now, if we had pension funds in this country anymore, they’d still hold stocks and bonds, sure, but their managers would not be incentivized to rack up more fees in lieu of providing stable returns for future retirees.

If you’re a CEO, and your company happens to be on an index or in an ETF that retirement fund mangers favor, this is very good news for you too. In the olden days, companies might have had to woo investors to buy and hold their stocks by running their companies well, offering amazing shareholder returns, or taking investors out to dinners and golf, I have no idea. Nowadays, if you are a ‘blue chip’ company, meaning your stock is in any of the large indexes, you have a steady stream of passive investor cash from large managed funds. The larger a retirement or index fund grows, the more of your stock it’s required to buy (as part of a big bucket of ‘good’ stocks) and voila, your company will continue to go up and to the right, unless you do massive accounting fraud or make fund managers uncomfortable with your antics.

America’s retirement economy is a pretty sweet deal for finance companies, and finance companies give a lot of money to lawmakers, which is why it’s no surprise they are constantly trying to privatize Social Security and give everyone investment accounts rather than a - say it with me - guaranteed benefit pension plan. This week a group of Senators applied a fresh coat of lipstick to that old pig:

The plan also includes a proposed sovereign wealth fund (as previously reported by Semafor) that could be seeded with $1.5 trillion or more in borrowed money to jumpstart stock investments, the people said. If it fails to generate an 8% return, both the maximum taxable income and the payroll tax rate would be increased to ensure Social Security stays on track to be solvent another 75 years.

Not content to funnel trillions of employee pay into private investment funds earning bankers billions in fees, the government wants to create a new fund to…buy more stocks? And if it fails to generate returns, we’ll punish working folks by raising payroll taxes, which would depress wages. You’ll notice they never propose raising the Social Security tax cap, which would actually impact rich people, and fund our country’s pension plan to boot.

We talked last week about how the rich are rich not because they invented something incredible, or cured a disease, or created a major good for society, but because they are able to take advantage of investment vehicles and - often - public markets to use other peoples’ money to inflate their own net worth. The US’s perverse retirement system actually makes it much, much easier for the wealthy to grow that wealth, because we’ve got a self-feeding financial system shoveling billions a year of wages into the smoldering landfill of public markets.

It feels cynical to point out that our retirement system resembles a pyramid scheme, and I assure you I do not relish the comparison. Just like our health care, insurance, and even the food we eat, American wealth is extracted from the bottom up, enriching a small number of elite families and corporations, smaller nuggets flaking off along the way to line the pockets of all the middlemen who keep the gears greased and the system running.

Drugs

This week, Eli Lilly bought itself some positive press by declaring it would reduce the prices of some of its insulin products. The cost of insulin in this country has been a Democratic talking point, with Bernie Sanders and Joe Biden hammering a greedy pharmaceutical industry constantly raising prices on a life-saving drug. Stories of diabetics rationing insulin and dying at the hands of corporate greed have been a reality among America’s poor and middle class for decades.

It’s not quite so simple as Lilly capping prices on all its insulin products, though:

In reality, though, Lilly’s moves are more limited than they initially appear. Lilly’s existing $35 cap on out-of-pocket payments will be easier for privately insured patients to take advantage of. But the policies announced Wednesday will not have much, if any, effect on what many people are actually paying.

[…]

And Lilly was already charging insurers only a fraction of its high list price when accounting for rebates and discounts.

If you’ve ever had a procedure or purchased expensive medicine through the American health insurance system, you may have received a bill showing some astronomical price, and an ‘adjusted’ price after insurance. It is dumb theater we allow drug companies and insurers to perform - if the insurance price was fifty bucks and not five thousand, why send a bill saying five thousand? The answer, of course, is that they send the bill saying five thousand to the tens of millions of people without health insurance, though insurers typically allow patients to negotiate that price down a bit. It is all extremely stupid and the fact we’ve become accustomed to it is deeply embarrassing.

Insulin is not the only drug susceptible to arbitrary price hikes to pad pharma company coffers. Two other drugs have earned their owners incredible wealth through a series of legal tricks, at patients’ great expense.

Last month, anti-inflammatory drug Humira lost its monopoly, and the market for arthritis treatment will finally have competition after twenty years. AbbVie, the company that owns the rights to Humira, has made a fortune blocking competitors from creating generics:

Through its savvy but legal exploitation of the U.S. patent system, Humira’s manufacturer, AbbVie, blocked competitors from entering the market.

[…]

Over the past 20 years, AbbVie and its former parent company increased Humira’s price about 30 times, most recently by 8 percent this month. Since the end of 2016, the drug’s list price has gone up 60 percent to over $80,000 a year, according to SSR Health, a research firm.

AbbVie used legal loopholes to give itself 6 more years of exclusivity with Humira, which cost Medicare alone an estimated $2.2 billion dollars more than it’d have paid for generic competitors. The company piled up a series of patents on the drug’s components, creating fresh legal challenges to copycats and earning the company approval to recommend the drug to treat other diseases.

Watching AbbVie earn an astounding $208 billion dollars on a single drug has encouraged other pharma giants to imitate its tactics - Amgen, Merck, and others are stacking reams of patents on popular drugs to extend the duration of their American monopolies.

Another company, Jazz Pharmaceuticals, used legally questionable tactics to protect its narcolepsy drug, contesting any challenge to its patents under obscure federal safety rules because regulators had forced the company to come up with extra safety precautions to avoid the drug being used in date rape:

Jazz took the unusual step of patenting that safety program and then listing those patents in a federal registry known as the Orange Book. Under an obscure federal rule, if a rival contested one of the patents in certain circumstances, federal regulators would be barred for more than two years from approving that competitor’s product.

Yes, the company with a dangerous date rape sleep drug patented the safety program for protecting people from date rape, and used that to maintain its lucrative patent monopoly. The sleep drug accounted for fifty-eight percent of the company’s revenue in 2021.

To make matters worse, the competitor product Jazz fought to keep off the market was much easier to take for narcolepsy, so Jazz’s profiteering made life worse for patients beyond its excessive cost. Arguably, any drug company keeping an expensive, older drug on the market is making life worse for patients, and racking up huge Medicare bills to treat arthritis does mean someone, somewhere may not get a treatment they need.

Along with yelling about insulin, Sanders and other progressives have long fought to allow Medicare to negotiate drug prices - they got a small victory in the Inflation Reduction Act, but its provisions only cover a small number of popular drugs. As long as pharma companies are allowed to manipulate the legal system to extend the length of drug monopolies, Medicare and health insurers (and poor patients) will deposit billions into the coffers of greedy pharma companies.

Crypto

Remember crypto? Barely a year ago every large company and bank was on about blockchain and crypto. Then a bunch of the major exchanges turned out to be Ponzi schemes, and others were actually insanely leveraged bets on volatile crypto markets that exploded, and now boring tradfi firms are like hang on, maybe we shouldn’t associate our brands with the Giant Fraud Marketplace:

Both Visa and Mastercard have decided to push back the launch of certain products and services related to crypto until market conditions and the regulatory environment improve, said the people, who asked not to be named as talks were confidential.

This is a good idea! When you are already the global payments duopoly, maybe you don’t want the reputational risk associated with being more overtly involved with international criminal networks and such.

Don’t worry, though, the two companies with a hammerlock on the world’s electronic payments are still hype about blockchain:

A spokesperson for Mastercard said: "Our efforts continue to focus on the underlying blockchain technology and how that can be applied to help address current pain points and build more efficient systems."

I mean, sure, if the global payments system was more efficient Visa and Mastercard could make even more money, so I understand their motivations. Until blockchain is something other than A Database, But Slower, I am not sure how it is helpful to them, but as long as they aren’t spending Meta Metaverse money on it, who cares I guess. Ah, crypto. Those were the days.

Short Cons

WIRED - “The Alonzo Sawyer case adds to just a handful of known instances of innocent people getting arrested following investigations that involved face recognition misidentification—all have been Black men.”

Insider - “The 2022 study found that Wall Street financial advisors with the worst histories of misconduct often switched to selling insurance after they got in trouble.”

ARS Technica - “On Friday, Getty filed a second lawsuit against Stability AI Inc to prevent the unauthorized use and duplication of its stock images using artificial intelligence.”

USA Today - “TD Bank and two other banks have agreed to pay a combined $1.35 billion to settle a lawsuit accusing them of aiding disgraced financier Allen Stanford’s $7 billion Ponzi scheme.”

Know someone considering filing anticompetitive patents to maintain a yearslong monopoly over a life-saving medication? Send them this newsletter!