Touch the Poop

Castoreum

After my post last week about brands mislabeling vanilla in their food, some helpful friends on Facebook informed me one source of artificial vanilla flavoring is anal secretions from beavers:

Technically called castoreum, there's a substance described as "brown slime" that comes from the beaver's castor gland, which is located a short gasp away from its anal gland, right there under its big tail.

Castoreum is so favorably fragrant that we've been using it to flavor ice cream, chewing gum, pudding and brownies -- basically anything that could use a vanilla, raspberry or strawberry substitute -- for at least 80 years.

It is a testament to human ingenuity that centuries ago, someone sniffed (and tasted) beaver ass juice and decided it made a good flavor and fragrance:

Because we humans have been using castoreum for so long, the name of the adventurous person to first put their nose into a beaver's butt (or in a beaver's sticky scent mound on the forest floor) has been lost to time.

But we know that the Romans burned castoreum in lamps because they thought the fumes caused abortions, and trappers have used it to lure animals since at least the 1850s.

Well, okay. In modern times, beaver slime was used to create artificial vanilla flavor. But! The…good? news is that it no longer is:

These days, castoreum is primarily used for fragrances, not foods. It's too expensive and cumbersome (and gross) a process to extract. A little less than 300 pounds is produced every year, which is stretched thin throughout the market.

Because it's considered safe, the FDA doesn't require companies to specifically say they're using castoreum. They can just say "natural flavoring."

But the chances castoreum is in your food are slim to none.

What a relief! However, the ingredients in the other artificial vanilla don’t sound too appetizing, either:

Vanillin can come from vanilla beans, but the process takes a lot of labor and land to produce, so chemists have gotten crafty in the materials they've used to make synthetic vanillin in a lab.

One of these many sources is ... coal tar.

[…]

Coal tar isn't the only thing that's been used to produce synthetic vanillin. Over the last century, cinnamon, paper waste, pine bark, and even cow poop has mimicked the taste and smell of real vanilla.

Come on, man! Why are human beings predisposed to a flavor that can be found in beaver ass, cow shit, paper waste, and coal tar? I don’t know. I still buy vanilla ice cream, and once I’ve erased this story from my brain, I will no doubt continue to do so.

Robert Smith

Smith, a private equity billionaire and the country’s richest Black man, made news in 2019 for surprising graduates at a commencement address by paying off their student loans. What reporters didn’t know at the time was that Smith was under investigation for a decades-long tax avoidance scheme that helped make him a billionaire in the first place:

U.S. prosecutors and Internal Revenue Service agents spent four years piercing the veil of secrecy that billionaire money manager Robert F. Smith wove to hide more than $200 million in income.

That’s a lot of money! So, what happened?

But rather than expose a man worth about $7 billion to a possible prison term and potentially force him to give up control of his private equity firm, Vista Equity Partners, Barr signed off on a non-prosecution agreement. It required Smith to admit he had committed crimes, pay $139 million and cooperate against a close business associate indicted in the largest tax-evasion case in U.S. history—Texas software mogul Robert T. Brockman.

Ahh, of course. When you reach a certain level of wealth you can simply harass the Attorney General of the United States until he cuts you a break.

Backing up, Smith got his start in private equity when Brockman offered to stake his first fund in exchange for Smith setting up a web of offshore entities and helping Brockman evade taxes. Time and again, Smith’s company Vista Equity Partners shuffled cash around the globe, avoiding the IRS and pocketing tidy profits.

The authorities caught wind of Smith’s tax schemes during a messy divorce - a year later Smith married a Playboy model - when his wife alluded to offshore assets. Between 2014 and 2019 Smith attempted to amend his prior tax returns and donated hundreds of millions of dollars to charity, but the authorities were undeterred. So, failing that, he cozied up to the Trump administration, going to events and appearing on television praising the senior members of the cabinet. His lawyers secured multiple meetings with AG Barr, which is a normal thing for a tax cheat to have access to:

Smith’s lawyers continued to push for a non-prosecution agreement, and the case went to Barr a second time, people with knowledge of the matter said.

[…]

In July, Smith’s team made a direct appeal to Barr, according to people with knowledge of the matter.

This was possible in large part because some of the lawyers representing Smith had once served at the Justice Department and the IRS. The rich - the only people who can afford insanely expensive tax attorneys - regularly make use of the revolving door, in this case going over the heads of prosecutors straight to their boss, the highest law enforcement official in the land. Smith believed his influence was so great he could avoid accountability entirely:

In the weeks leading up to the announcement, Smith had pressed his legal team to obtain an assurance that the government wouldn’t publicly disclose his misconduct, people familiar with the matter said. The request was denied.

Anyhow, Smith has to pay a fraction of his fortune and cooperate and testify against his old benefactor, who’s facing the largest tax fraud case in history. Brockman’s got a different defense in mind - that he’s unfit to stand trial:

That effort may not include taking the witness stand against Brockman, who stepped down as chief executive officer of Reynolds & Reynolds in November. His lawyers said in court that the 79-year-old is suffering from dementia. They said the case should be dismissed because he’s unable to assist in his own defense.

Prosecutors characterized the timing of the claim as suspicious and urged the court to regard it with “healthy skepticism.” A federal judge in Houston will decide if he’s competent to stand trial in the coming months.

Again, if you have unlimited funds and attorneys who know the right people, no legal argument is too ridiculous or unlikely to succeed.

Chinese Microlending

I’ve written a little about microlending - a phenomenon mostly confined to developing countries with large numbers of unbanked citizens. What I didn’t realize, however, was that microlending is common in China, where all the major tech firms integrate loan services into their apps:

Of the 20 most commonly used apps in China — ranging from photo editing to file sharing, from maps to streaming platforms — all have some kind of in-app loan services, according to Chinese tech site iFanr.

The growth of Chinese fintech platforms really turbocharged around 2015, said David Yin, vice president and senior analyst at Moody's financial institutions group. "Financial innovation was encouraged at that time, with very loose regulatory requirements," he told Protocol.

Imagine if Instagram or Uber Eats were constantly trying to lend you money. It’d be a real pain, but that’s exactly what the average Chinese consumer is dealing with these days. It’s easy to forget that China has not been a wealthy, modern nation for very long, and its massive population means wealth distribution has taken time to catch up, especially for younger generations:

"The low penetration of traditional banking services provided an opportunity for the tech companies to step up and meet customers' credit needs," Sharma Nariyanuri said. For the generation that grew up with smartphones, going to an online credit service like Jiebei is more natural than applying for a credit card.

As is common with unsecured lending, interest rates can very quickly get out of control, with companies clamoring to loan consumers more money to pay off their existing loans, raking in annual interest rates as high as 36%, the country’s legal limit - in some US states payday lenders can charge twenty times that.

The good news is China’s financial regulators have taken an interest in microlending and may step in to dramatically curtail it - cutting off a revenue stream for many of the Chinese tech giants, and helping protect consumers from endless predatory loan advertisements and gross, aggressive collections tactics:

There are countless complaints on social media about debtors being bombarded with calls, texts and WeChat messages, some even sent to their colleagues and friends, pressing them to pay loans back.

Citigroup

This week a federal judge in New York handed down a surprising verdict, ruling that Citigroup could not recoup $500 million dollars it mistakenly sent to a group of creditors for the cosmetics company Revlon. The ruling and much of the debate around it is very lawyerly and financey and I’ll let you read that on your own if you so desire. What I want to talk about is how it happened. How does a bank accidentally wire $900 million dollars? That story is delightfully stupid:

Three employees working for Citigroup Inc. told a federal judge they made errors in processing an interest payment that resulted in the mistaken transfer of $900 million to Revlon Inc. lenders.

Details of the blunder were revealed as the workers took the stand on the first day of a trial in which the bank is seeking to recover more than $500 million from recipients that say they were owed it.

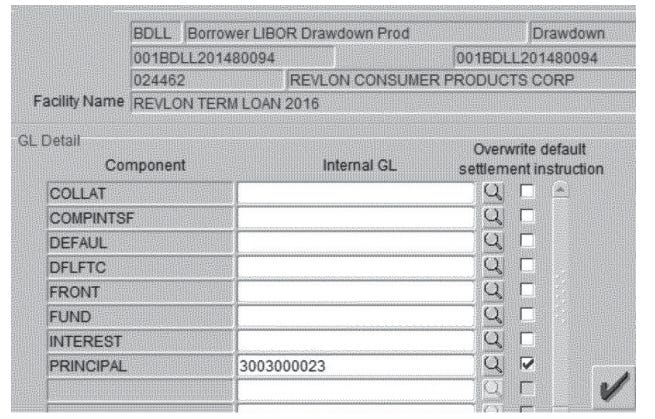

Getting the financey bit out of the way - Revlon had a bunch of debt, and it did some…creative debt restructuring that didn’t sit well with all of its creditors. In the process it’s bank, Citigroup, had to use its computer systems to roll the debt and interest payments into a new structure. Enter Flexcube, Citi’s internal payment software:

On Flexcube, the easiest (or perhaps only) way to execute the transaction — to pay the Angelo Gordon Lenders their share of the principal and interim interest owed as of August 11, 2020, and then to reconstitute the 2016 Term Loan with the remaining Lenders — was to enter it in the system as if paying off the loan in its entirety, thereby triggering accrued interest payments to all Lenders, but to direct the principal portion of the payment to a “wash account” — “an internal Citibank account that shows journal entries . . . used for certain Flexcube transactions to account for internal cashless fund entries and . . . to help ensure that money does not leave the bank.”

Anyone who’s used accounting software, or really any software at their job, is probably groaning right now. We’ve all likely encountered some version of Flexcube - software that doesn’t really do what you want it to, but someone in IT has figured out a workaround if you just click a few extra things or trick the software into doing something it doesn’t want to. So, Citi’s software couldn’t restructure the loans without paying out interest and principal, but Revlon didn’t want to pay the principal on the loans, so Citi’s software was supposed to pretend it was paying the principal, and it would end up in a “wash” account that never left the bank. So, what happened next?

When entering a payment, the employee is presented with a menu with several “boxes” that can be “checked” along with an associated field in which an account number can be input.

[…]

Raj then proceeded with the final steps to approve the transfers, which prompted a warning on his computer screen — referred to as a “stop sign” — stating: “Account used is Wire Account and Funds will be sent out of the bank. Do you want to continue?” But “[t]he ‘stop sign’ did not indicate the amount that would be ‘sent out of the bank,’ or whether it constituted an amount equal to the intended interest payment, an amount equal to the outstanding principal on the loan, or a total of both.”

Uh oh. So the unfortunate Citi employee(s) handling the transaction intended for the interest payments to be sent and the principal of the loans - $900 million dollars - to stay in the bank. But they checked the wrong boxes and the stop sign didn’t tell them how much money they were sending. I am cringing internally as I read what happened to the poor sap the next day:

Fratta then forwarded the same email to members of his team, with the subject line “Urgent Wash Account Does not Work.” He stated: “Flexcube is not working properly, and it will send your payments out the door to lenders/borrowers. The wash account selection is not working.

Yeah, we’ve all been there. Blame the software! Flexcube is broken! Then, over the course of the day, the team realized that they hadn’t checked two of the boxes needed to trick the software into sending the money to the internal bank account and, well, shit.

Anyhow, $500 million of the total went to hedge funds who were not happy about Revlon’s financial shenanigans and they simply told the bank “no” when it asked for the funds back. Citigroup sued them, saying they had to pay the money back, and a judge ruled they didn’t have to, because the amounts were the legal repayment of the loan and besides, Citi hadn’t immediately informed them the wires were sent in error because it didn’t even notice until the next day due to its bad software.

I seem to be writing about topics with no clear hero lately, and this is another one. Do I feel bad for Citigroup, a bank with trillions in assets? Am I happy that some hedge funds got their money back because a bank employee screwed up? I don’t know. I feel terrible for the bankers who botched the transfer, because they are almost certainly going to be fired and maybe get in legal trouble - I hope not! They will undoubtedly be the scapegoats when, really, the problem is that the nation’s biggest bank has very bad banking software and the executives who forced its employees to continue to use it should be fired and forced to work in IT.

Stonks

I haven’t written about stock markets in a few weeks and, frankly, it feels good. But there is this piece in the WSJ talking about how “outsiders” - people who do not explicitly work in finance - are now driving stock and crypto prices just by tweeting and saying things and, ugh, fine:

Thus, today’s outsiders are signaling to everyday investors what should have been obvious for a long time. “The internet has democratized information,” Mr. Palihapitiya told me this week. “So the edge has shifted to analysis. Everyone has access to the same information, financial disclosures and general data.”

That erases Wall Street’s illusion of superior knowledge. “The stagnation of traditional wages has shifted people’s resourcefulness to the equity markets,” said Mr. Palihapitiya. Those who can use technology “to process this information faster or differently,” he said, have “the new edge.”

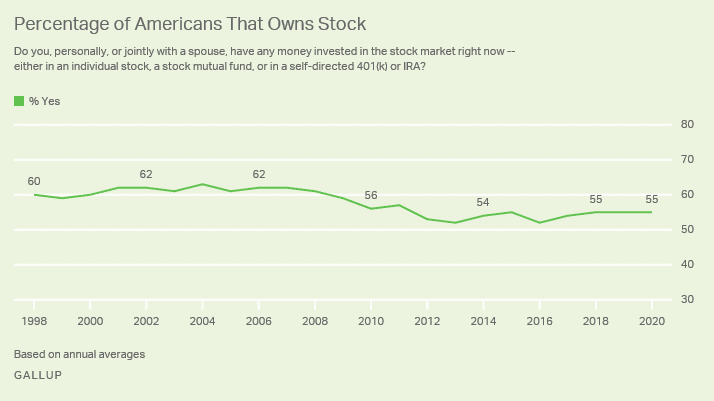

Huh? What is he talking about? According to Gallup, stock ownership is down almost 10% in the last 20 years:

However, rich investors like Palihapitiya can use Twitter to juice stocks they’ve just purchased, so I guess uh, people spending what little disposable income they have on meme stocks does work out well for him?

Also, two paragraphs before that, the article discusses The Big Finance Lie - the people who previously moved markets with their Serious Opinions - delivered in newspaper columns or investor reports - don’t know anything either:

Not long ago, analysts such as Mary Meeker and Jack Grubman, and strategists such as Abby Joseph Cohen and Barton Biggs, were superstars. Analysts, economists, strategists and portfolio managers still play the roles of clairvoyants, even though they are just guessing like the rest of us.

Here’s a quote from Mark Cuban, a billionaire who has been actively pumping stocks and cryptocurrency on any platform that’ll give him a microphone:

Historically, most traders have lost money, conceded Mr. Cuban. But “this may be the one set of circumstances that could change all that.” Could more people profit if “first-time or newer traders [and] veteran traders chose to work together instead of individually?” he asked. “Why can’t that knowledge come from the wisdom of the crowd?”

I don’t know, Mark, because even the collective might of Reddit can’t compete with hedge funds and trading desks with billions of dollars to throw around? You moron? Whatever. We’re still in the middle of a pandemic and if people want to mess around with all the money they’re saving by never leaving the house, I’m fine with it.

Matt Levine points out that despite the best efforts of journalists, they haven’t been able to find anyone who truly got wiped out in the Meme Stock Craze of January 2021. In fact it’s mostly just people doing it for fun, or out of boredom. Which, again, is fine. People can do whatever they want with their money. I wish we focused their attention more on the rich people manipulating markets for their own profit, but I get it, there’s a lot going on right now.

Short Cons

TechCrunch - “…the consumer watchdog found that Google’s presentation for classifying tourist accommodation — including identical use of the term “stars” on the same scale from 1 to 5 — to be confusing for consumers.”

The Cut - “The Wing was a triumph of branding that succeeded until the contradictions at the heart of its brand became untenable, which happened in 2020.”

WaPo - “The latest indictment shows the degree to which North Korea relies on financial cybertheft to obtain hard currency in a country whose main exports are under United Nations and U.S. sanctions, and that is further isolated by a self-imposed coronavirus blockade.”

WaPo - “Meanwhile, some of their colleagues were working undercover to expose the long-running scheme responsible for the lavish spread, and tipping off federal authorities to a world of clandestine after-hours meetings at state laboratories and five-gallon buckets filled with gleaming fish roe.”

Tips, thoughts, coal tar ice cream to scammerdarkly@gmail.com